Choosing the right life insurance can be confusing. Two options stand out: term life insurance and whole life insurance. People often wonder which is better for their needs. This choice matters because it affects your family’s financial safety, your long-term plans, and even your budget. By understanding the main differences, pros, and cons, you can make a smarter decision that gives you peace of mind.

What Is Term Life Insurance?

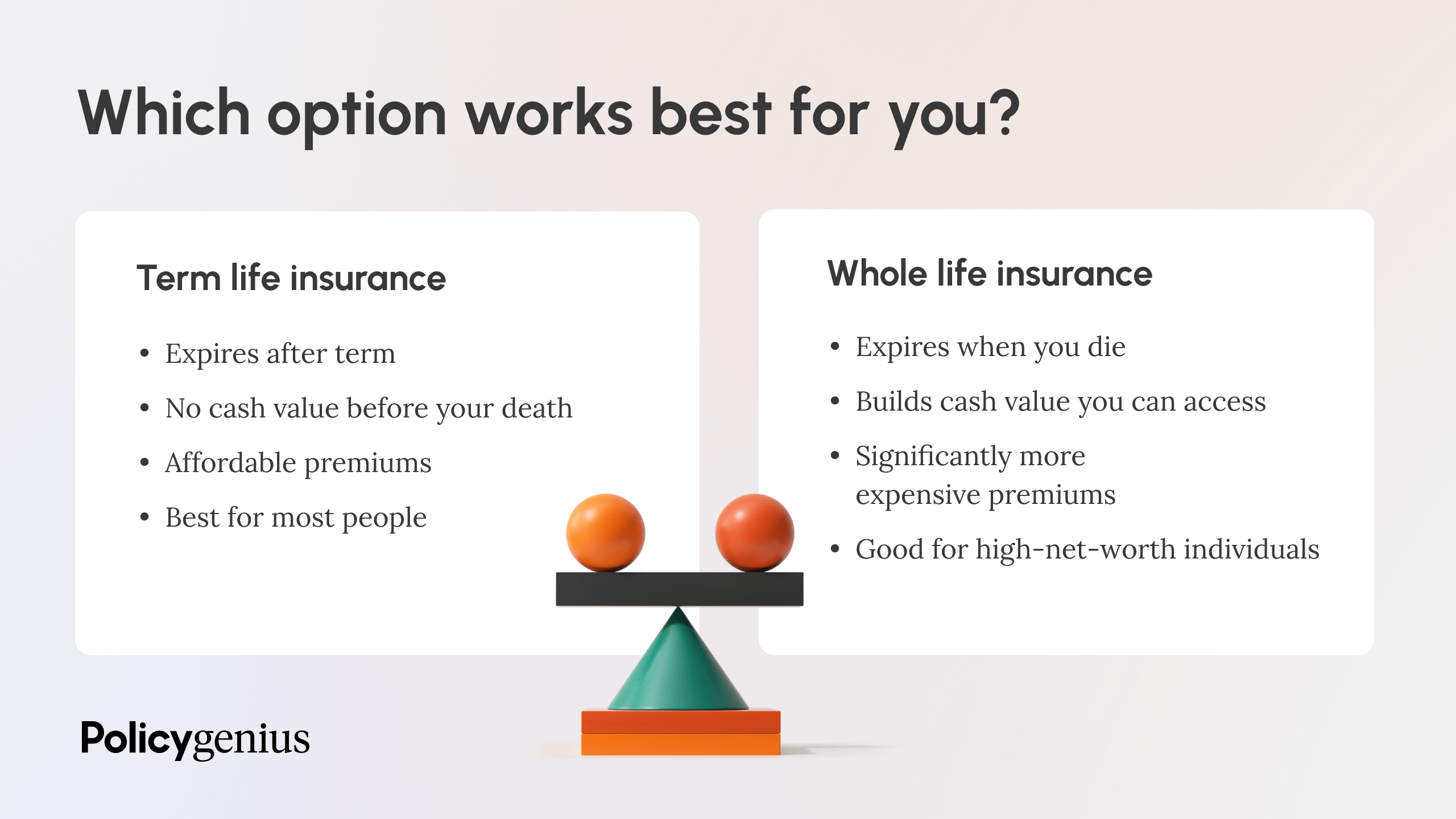

Term life insurance is a policy that covers you for a set period, such as 10, 20, or 30 years. If you pass away during this time, your beneficiaries receive a payout. If you outlive the term, the policy ends, and there’s usually no cash value or payout.

One reason many people choose term life is the affordable premiums. For example, a healthy 30-year-old non-smoker might pay just $25–$30 per month for $500,000 of coverage over 20 years. The cost is low because most policies never pay out—the majority of people outlive their term.

Common uses of term life insurance:

- Protecting your children until they become financially independent

- Covering a mortgage or debts that will end in a set number of years

- Providing income replacement during your working years

Many employers offer group term life as a benefit, but the coverage is often limited. Buying your own policy gives you more control and coverage.

What Is Whole Life Insurance?

Whole life insurance is a type of permanent life insurance. It lasts for your entire life as long as you pay the premiums. When you die, your beneficiaries get the payout no matter when that happens.

A key feature is the cash value: part of your premium goes into a savings component. This cash value grows over time, and you can borrow against it or withdraw funds in certain situations. Premiums are much higher than term life, but the policy builds value over decades.

Whole life insurance is often used for:

- Lifetime financial protection for loved ones

- Estate planning and covering inheritance taxes

- Creating forced savings for future needs

For example, a 30-year-old non-smoker might pay $350–$400 per month for a $500,000 policy. The cash value might total tens of thousands after 20 years, depending on the policy and investment performance.

Main Differences Between Term And Whole Life

Understanding the core differences helps you see which fits your situation. Here’s a clear look at the biggest contrasts:

| Feature | Term Life | Whole Life |

|---|---|---|

| Coverage Period | Set term (10, 20, 30 years, etc.) | Lifetime (permanent) |

| Premiums | Lower, fixed for term | Higher, fixed for life |

| Cash Value | None | Yes, grows over time |

| Payout Guarantee | Only if death during term | Guaranteed, whenever you die |

| Flexibility | Can renew or convert (sometimes) | Locked in, but loans/withdrawals possible |

Pros And Cons Of Term Life Insurance

Benefits

- Lower cost: For most people, term life is highly affordable, making it easier to get enough coverage.

- Simple structure: The policy is straightforward—if you pass away during the term, your family gets paid.

- Large coverage amounts: You can buy higher coverage amounts for less money compared to whole life.

Drawbacks

- Expires: If you outlive your term, you lose coverage and get nothing back.

- Premiums rise with age: If you renew or buy a new policy later, costs can jump, especially after age 50.

- No cash value: You can’t borrow or withdraw from the policy.

Pros And Cons Of Whole Life Insurance

Benefits

- Permanent protection: No matter when you die, your family receives the death benefit.

- Cash value grows: The savings component builds up tax-deferred, and you can access it for loans or emergencies.

- Level premiums: Your payments stay the same for life, so you can plan your budget.

Drawbacks

- Expensive premiums: Costs can be 5–10 times higher than term life for the same coverage.

- Slower cash growth: In the early years, cash value grows slowly because of fees and commissions.

- Complexity: Policies can be confusing, with many rules about loans and withdrawals.

How To Decide: Key Factors To Consider

Your choice depends on your goals, financial situation, and stage of life. Here are the most important things to think about:

1. Your Budget

- If you need high coverage for a low cost, term life is usually best.

- If you can afford higher premiums and want long-term value, whole life could work.

2. Coverage Needs

- If your main goal is to protect family during key years (e.g., until kids graduate), term life matches that need.

- If you want lifelong coverage (for example, to cover funeral costs or estate taxes), whole life is better.

3. Savings Goals

- If you want insurance plus a forced savings plan, whole life offers both.

- If you prefer to invest or save money separately, term life and separate investments may be smarter.

4. Age And Health

- Younger, healthy buyers get the best rates for either type.

- Waiting too long can make both types much more expensive or even impossible to get.

5. Other Insurance Or Financial Plans

- If you have strong savings, investments, or a pension, you might need less life insurance.

- If you have little saved, insurance becomes more crucial for your family’s security.

Credit: www.ramseysolutions.com

Real-life Examples

Sometimes, examples make the differences clearer.

Example 1:

Maria, age 32, just had her first child. She wants to make sure her child is safe if something happens to her. Maria chooses a 20-year term policy for $750,000. Her premium is $28/month. If she outlives the policy, the coverage ends, but by then, her child will be an adult.

Example 2:

James, age 40, owns a small business and wants to provide money for his heirs to pay estate taxes or keep the business running if he dies. He buys a whole life policy for $500,000 at $400/month. After 25 years, his policy has built $80,000 in cash value, which he can use for emergencies.

Non-obvious insight: Some people buy both types. For example, you might buy a large term policy for family protection and a small whole life policy for final expenses. This combination can balance cost and coverage.

Cost Comparison: Term Vs Whole Life

How much do these policies really cost? Here’s a simplified look for a 35-year-old non-smoker buying $500,000 in coverage:

| Policy Type | Monthly Premium | Total Cost Over 20 Years | Cash Value After 20 Years |

|---|---|---|---|

| Term Life (20 Years) | $27 | $6,480 | $0 |

| Whole Life | $380 | $91,200 | $45,000 (approx.) |

Important: The cash value in whole life policies depends on the insurer, the exact policy, and market conditions. Early years build value slowly.

Common Mistakes When Choosing

- Focusing only on price: Low premiums matter, but check if the policy truly meets your needs.

- Ignoring the fine print: Some term policies don’t allow conversion to permanent insurance. Some whole life policies have high surrender charges.

- Over-insuring or under-insuring: Buying too much coverage wastes money; too little leaves your family at risk.

- Assuming you can always renew: Health changes or age may make new policies impossible or very expensive.

- Thinking cash value is easy to access: Loans from whole life policies reduce the death benefit and may have interest.

When Term Life Is Usually Better

- You need coverage only for a specific period (kids in school, mortgage years)

- Your budget is tight, but you want maximum protection now

- You plan to invest the savings from lower premiums elsewhere (like a 401(k) or IRA)

Term life fits most young families, new homeowners, and people early in their careers. You can often convert some term policies to whole life later, but always check the details.

When Whole Life Is Usually Better

- You want insurance that never expires, no matter what

- You have complex estate planning needs (e.g., business succession, leaving a legacy)

- You like the idea of building a cash value you can access

Whole life works best for high earners, people with large estates, or those who want permanent life insurance and are willing to pay more.

Not-so-obvious Insights

- Policy loans are not free: When you borrow from your whole life cash value, you pay interest, and unpaid loans reduce the death payout. Many people misunderstand this and think they’re “borrowing from themselves” without cost.

- Dividends are not guaranteed: Some whole life policies offer dividends, but these are based on insurer performance and can change year to year.

Should You Mix Term And Whole Life?

Some financial planners suggest a mix. For example, you might buy a large term policy for 20–30 years (to cover your family) and a small whole life policy to cover funeral costs or leave a small legacy.

This approach can give you both affordability and some permanent coverage. However, be sure you understand the costs and benefits, as mixing policies adds complexity.

How Insurance Companies Make Money

Many people wonder why whole life is so much more expensive. Insurers price term life low because most policies never pay out. With whole life, the company knows it will pay a claim eventually, so it charges more and invests the cash value.

Insurers also earn from investment returns and policy fees.

For more on how insurance works, check out this Wikipedia article on life insurance.

Credit: www.westernsouthern.com

Which Is Better For You?

There is no one-size-fits-all answer. The right choice depends on your life stage, family situation, and financial goals. Most people start with term life for high, affordable coverage. Whole life makes sense if you want permanent protection and are comfortable with higher payments.

If you’re still unsure, talk to a fee-only financial advisor. Avoid agents who push one type over the other just for higher commissions.

Frequently Asked Questions

What Happens If I Outlive My Term Life Policy?

If you survive the term, your coverage ends and there is no payout. Some policies let you renew or convert to whole life, but premiums will be higher.

Can I Cash Out My Whole Life Insurance Policy?

Yes, you can withdraw or borrow from the cash value. However, withdrawals may reduce your death benefit and could have tax consequences.

Is Whole Life Insurance A Good Investment?

Whole life has a forced savings feature, but returns are usually lower than other investments like stocks or mutual funds. It’s best for those who want permanent coverage and conservative growth.

Can I Switch From Term To Whole Life Insurance Later?

Some term policies allow conversion to whole life without a new health exam, but only during a certain period. Always check your policy details.

How Much Life Insurance Do I Need?

A common rule is 10–15 times your annual income, but your needs may vary. Consider debts, children’s education, and your family’s living expenses.

Choosing between term and whole life insurance is a big decision, but understanding the basics helps you protect what matters most. Make sure to review your needs regularly, as life changes can affect the best policy for you.

Credit: www.policygenius.com

Read More:

- Third-Party Vs Comprehensive Car Insurance: Which Is Best?

- Do You Really Need Life Insurance? Key Facts You Must Know

- What Affects Your Car Insurance Premium? Key Factors Explained

- How to Lower Your Car Insurance Cost: Proven Tips That Work

- How Much Life Insurance Should You Have? Essential Guide 2024

- How to Pick the Best Health Insurance Plan: Expert Tips

- What Does Health Insurance Actually Cover? Essential Facts Explained

- How Health Insurance Works in Simple Terms: Easy Guide