Choosing the right amount of life insurance is one of the most important financial decisions you can make. It affects your family’s future, their ability to pay bills, and their peace of mind if you pass away. But how much is enough?

Too little life insurance leaves your loved ones struggling. Too much means paying more than needed. This article will help you understand how to calculate the right amount, what factors matter, and avoid common mistakes—using simple, clear explanations for everyone.

Why Life Insurance Matters

Life insurance is not just for the wealthy or elderly. It is a safety net for anyone with dependents or debts. If you have children, a spouse, or parents relying on your income, your absence could cause financial hardship. Even single people may need coverage for funeral costs or to settle debts.

A 2023 survey by LIMRA found that 44% of US households would face financial trouble within six months if the primary wage earner died. That’s why having the right life insurance coverage is so important.

Key Factors That Influence Your Life Insurance Needs

Several factors affect how much life insurance you should have. Let’s look at each:

- Income replacement: How much money your dependents need to maintain their lifestyle.

- Debt coverage: Mortgage, car loans, credit cards, and other debts.

- Education costs: College funds for children.

- Final expenses: Funeral and burial costs.

- Existing assets: Savings, investments, or other insurance.

Each factor is unique to your situation. For example, a family with young children and a mortgage needs more coverage than a single person with no debts.

Estimating Your Life Insurance Needs

There are several ways to estimate how much life insurance you need. Here are the most common:

The Income Multiplier Method

One simple rule is to multiply your annual income by a number between 7 and 10. For example, if you earn $50,000 per year, you may need $350,000 to $500,000 in coverage. This method is easy but does not consider your debts or assets.

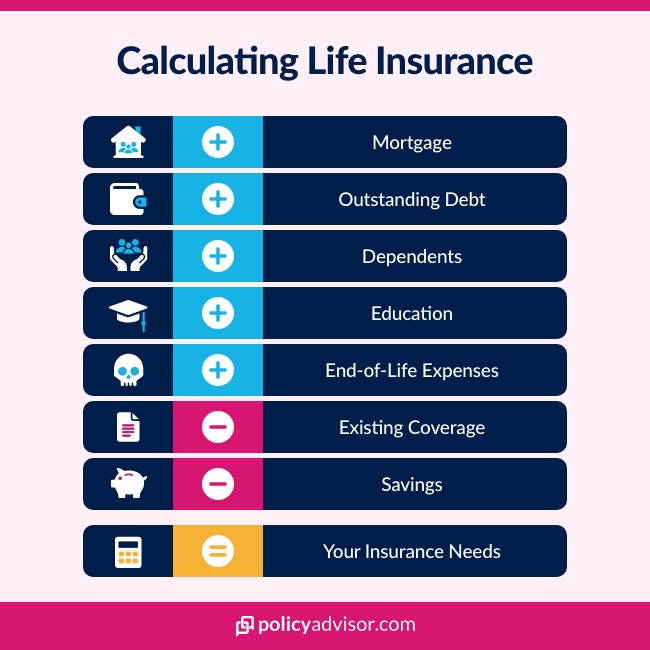

The Dime Formula

DIME stands for Debt, Income, Mortgage, and Education. Add these together to get a more accurate estimate.

- Debt: Total personal debts and funeral costs.

- Income: Years your family will need income replacement × your annual income.

- Mortgage: Remaining mortgage balance.

- Education: Estimated college costs for each child.

For example, suppose:

- Debt = $15,000

- Income = $50,000 × 10 years = $500,000

- Mortgage = $200,000

- Education = $50,000 × 2 children = $100,000

Total Coverage Needed: $815,000

Needs-based Analysis

This method looks at your family’s actual expenses and assets. Subtract your assets (like savings and investments) from your total needs to find the coverage gap.

| Category | Amount |

|---|---|

| Income Replacement (10 years) | $500,000 |

| Debts & Mortgage | $215,000 |

| Education (2 children) | $100,000 |

| Final Expenses | $15,000 |

| Total Needs | $830,000 |

| Existing Assets | $100,000 |

| Coverage Needed | $730,000 |

This approach is more precise and fits your personal situation.

How Age And Life Stage Affect Your Coverage

Your life insurance needs change as you age. A young parent with small children usually needs more coverage than someone near retirement. Let’s compare typical needs by age group:

| Life Stage | Typical Needs | Why? |

|---|---|---|

| 20s–30s (Young families) | High coverage | Children, mortgage, debts |

| 40s–50s (Established career) | Medium coverage | Fewer debts, children’s college |

| 60s+ (Retired) | Low coverage | Income replacement less needed, focus on final expenses |

Adjust your coverage as your life changes. For example, if your children finish college or you pay off your mortgage, you may need less insurance.

Credit: www.ramseysolutions.com

Types Of Life Insurance: Term Vs. Whole Life

The amount of life insurance you need also depends on the type of policy you choose. There are two main types:

Term Life Insurance

- Covers you for a set period (10, 20, or 30 years)

- Usually cheaper and gives higher coverage

- Best for covering debts, income replacement, and education costs

Whole Life Insurance

- Covers you for your entire life

- More expensive, but builds cash value

- Useful for estate planning, leaving inheritance, or final expenses

Most people use term life for big needs and whole life for smaller, permanent needs.

Common Mistakes When Buying Life Insurance

Many people make mistakes when choosing life insurance. Here are some to watch out for:

- Guessing the amount needed without doing the math

- Ignoring inflation (costs may rise over time)

- Not updating coverage as life changes

- Overestimating assets (some assets may not be liquid or accessible)

- Underestimating expenses (like college costs or medical bills)

A non-obvious mistake: Many people forget about taxes or legal fees that may reduce what beneficiaries receive. Always check with an advisor about these hidden costs.

:max_bytes(150000):strip_icc()/insureneeds.asp-final-4b172e0dd7db4fc585b5500870cbb899.png)

Credit: www.investopedia.com

How Much Is Enough? Real-world Examples

Let’s look at two real-life situations:

- Single parent, two children: Needs high coverage to replace income, pay mortgage, and cover education. If annual income is $60,000, mortgage is $150,000, debts are $10,000, and college for two kids is $80,000, total coverage needed is about $740,000.

- Retired couple, no dependents: Only needs coverage for funeral costs and small debts. If final expenses are $15,000 and debts are $5,000, coverage needed is just $20,000.

Both cases show that there is no “one-size-fits-all” answer.

How To Review And Update Your Life Insurance

Life insurance is not a “set it and forget it” decision. Review your coverage every few years or after big life events:

- Getting married or divorced

- Having children

- Buying a home

- Changing jobs

- Retiring

If your financial situation improves, you may need less insurance. If you take on new debts or have more dependents, increase your coverage.

Comparing Life Insurance Quotes And Policies

It’s important to compare policies before buying. Insurers offer different rates and features. Here’s a simple comparison of two term life policies:

| Policy | Coverage Amount | Term Length | Monthly Premium | Extra Features |

|---|---|---|---|---|

| Policy A | $500,000 | 20 years | $30 | Accidental death benefit |

| Policy B | $500,000 | 30 years | $45 | Disability waiver |

Compare coverage, term length, price, and extra benefits. Don’t focus only on cost; look at what matters most for your family.

Two Insights Most Beginners Miss

- Future earning power: Many people forget to insure not just their current salary, but their expected future earnings. If you are young and expect salary increases, your coverage should reflect that.

- Non-working spouses: Even if a spouse does not earn income, they may provide childcare or other services. If they pass away, you may need to pay for daycare, cleaning, or transportation. Include these costs in your coverage calculation.

Where To Get Reliable Life Insurance Advice

Getting advice from an independent financial planner can help. Don’t rely only on insurance agents—they may push products that give them higher commissions. For more information, check resources like NerdWallet.

Frequently Asked Questions

How Often Should I Review My Life Insurance Policy?

You should review your policy every 2–3 years or after any major life event (marriage, birth, new job, etc.). This helps keep your coverage up to date.

Can I Have More Than One Life Insurance Policy?

Yes, you can own multiple policies. Many people have a term policy for large needs and a small whole life policy for permanent coverage.

Is Life Insurance Payout Taxable?

Generally, life insurance payouts are not taxed for beneficiaries. However, if the policy is part of your estate, there may be estate taxes. Check with a tax advisor for details.

How Does Inflation Affect Life Insurance Needs?

Inflation can reduce the value of your payout over time. If you buy a $500,000 policy today, it may not cover as much in 20 years. Some policies offer inflation riders.

What Happens If I Can’t Pay My Premiums?

If you miss payments, your policy may lapse or end. Some policies offer a grace period or can be converted to a smaller policy. Always ask your insurer about options if you’re struggling.

Choosing the right amount of life insurance is about balancing needs and costs. It is not a fixed number—what’s right for you depends on your income, debts, assets, family, and future plans. Take the time to calculate carefully, review your coverage regularly, and ask for expert advice.

By doing this, you protect your loved ones and give yourself peace of mind for the years ahead.

Credit: www.policyadvisor.com

Read More:

- Third-Party Vs Comprehensive Car Insurance: Which Is Best?

- Term Vs Whole Life Insurance: Which Is Better for You?

- Do You Really Need Life Insurance? Key Facts You Must Know

- What Affects Your Car Insurance Premium? Key Factors Explained

- How to Lower Your Car Insurance Cost: Proven Tips That Work

- How to Pick the Best Health Insurance Plan: Expert Tips

- What Does Health Insurance Actually Cover? Essential Facts Explained

- How Health Insurance Works in Simple Terms: Easy Guide